Fun bedtime story: the systemic shock of this downturn causes investors to do what they are naturally prone to do, which is become fearful. Money dries up for the most speculative investments first, which removes the flow of dumb money from late-stage unicorn rounds.

Unable to raise further "growth capital" at attractive valuations, and burning money like there's no tomorrow, we see the first unicorn layoffs within 3 months. This spooks investors further, which dries up whatever funding was left for early stage deals. Within 6 months, the weakest startups are beginning to fail outright, which pulls back the tide a bit, and reveals the ponzi scheme of startup-servicing-startup revenue cycles for what they are. Suddenly, a number of heretofore assumed "safe" investments with "strong" revenues are revealed to be precarious, as 95% of their revenue streams were correlated.

Companies go from healthy revenue to practically nothing overnight, as dozens of companies all cut back on burn simultaneously. This only exacerbates the cash flow problems, and startups that were flying high are now flying into the ground at remarkable speed. Market gurus are revealed to be wearing no pants.

Within a year, the valley is in full recession, and people are clamoring for U-Hauls out of San Francisco, which are in short supply...

(In case you were wondering, this is essentially what happened in 1999, minus a few wild-cards like companies with totally fictional revenue, and companies that had no revenue at all.)

One major difference is that large parts of the internet are economically viable, and not just driven by money pumped in by VCs and IPOs. Back in 2000, there was little real consumer money going into the web's money cycle. Google didn't even have Adwords back then!

Of course there's still a large chunk of revenue today that is just recycling VC money - e.g. apps advertising in other apps, or AWS which is a huge sink of VC money from other startups. But there is a lot more "end user" money coming in from real people and companies that purchase products and services online. Even if that flow stops, the internet today is less of a ponzi scheme as a whole.

You're right that there's more legitimate internet revenue than in 2000. But most of that is going to a few established players that are decidedly post-unicorn in nature. I don't think Google is going anywhere (though Twitter might just get its fatal wound; that would be a particularly symmetrical ending, wouldn't it? Company born of the ashes of dot-com 1.0 dies in the explosion of dot-com 2.0. But, I digress.)

From what I know, most of the "unicorns" are neither profitable nor particularly modest with their spending. They are vulnerable to any sort of turn in investor sentiment, even if their revenue streams are real.

The key is that allegedly "overvalued" companies (like Uber say)are still under private investment which has a larger appetite for risk. Whereas in the last boom, most of the speculation were fueled by publicly traded tech stocks.

But privately owned companies are now funded largely by private equity who are massively leveraged. They will be first to the exits. IPOs meant the pain was more spread around among stock holders. Now the pain will be more concentrated among highly indebted leveraged investors. It won't end prettily.

It is a bit misleading to label all private equity as "massively leveraged." None of the major investors in "unicorns" of VC use leverage (e.g. Uber https://www.crunchbase.com/organization/uber/investors). In fact, the typical VC fund is legally barred from using leverage in their investments.

The buyout side of the PE market is leveraged, however, the investments in those investors' portfolios typically have big balance sheets to support the debt loads (and the interest payments).

I'm a bit new to the whole lingo of The Valley. Could you explain a little more verbosely what you meant by that sentence? What is beta capital and beta investments? What is considered high? What denotes a boom and what is an unwind? How bad is a killer unwind, what does that mean really? Again, sorry, trying to learn the fast lingo here.

Beta is a coefficient that attempts to measure an investment's likelihood to move 'with the market.' The total market has a Beta == 1 by definition, with beta ratings above 1 indicating higher volatility/sensitivity to market movements, and vice-versa. See Wikipedia for how the calculations are made.

In this context, I a 'high beta investment' is likely to move with the market, ie) is dependent on some aspect of market performance. 'Beta capital' I think refers to using sources of capital that are likely to become more or less available depending on the market. I've never heard of capital sources being given beta values though, so I think this may be a finance/VC colloquialism rather than an actual calculated value.

Disclaimer: I am not a VC and may be totally wrong.

jkimmel explained what beta is. The Tech industry as a whole has a high beta, and the smaller loss making component (i.e unicorns) an even higher beta. I am using the term beta loosely here as most of the unicorns are not public so they don’t really have a true beta, but they do have a pseudo-beta. They are being funded by private equity funds in what are effectively private IPOs.

The problem is that private equity funds are a high beta asset class. In times of risk aversion investors pull their money out of high risk asset classes and put them into lower risk asset classes like large public companies and bonds. Relatively small changes in investor preferences can get amplified up the investment chain resulting in large swings in demand at the far end.

A hypothetical example might be 10% of investors pull their money out of private equity funds, the funds find that most of their money is locked up in illiquid assets like loss making high growth tech companies (i.e. unicorns). In order to return the 10% of capital requested they have to cut new investments by 50%. The unicorns find that they are not able to raise the money they need to expand at the pace they have been and so go on a crash program to achieving profitability. They lay off developers, cut back on outside services, and stop buying small start-ups. VCs and angel investors seeing this cut back on investing stop putting money into new firms further decreasing demand. All of this is not good if you are running (or wanting to start) a business based on rapid growth that needs lots of capital.

Yeah, of course, there's a real valuation bubble going on. I don't think we'll see twitter going anywhere, too - it's a good product after all. But maybe returning to its real size in terms of worth, number of employees and spending.

Small, early stage companies (say <100 employees, <250m valuation) that high profile investors are competing to get in on? If so, most of them are supposed to fail. The money is still small by systemic standards and so are the number of people affected. Volatility here is not dangerous, it's expected.

Or, are you talking about the Unicorns expected to go public any day now? The Ubers and AirBnBs? Thee are also kind of retrospectively Unicorns at this stage. If these guys go under, that's a problem. But, these guys aren't rely reliant on investor sentiment.

Google didn't, but banner ads were around back then, and they were one of the main ways of making money off the Internet until the market bottomed out. DoubleClick was a pretty major player for years before Google bought them.

I remember lots of websites saying they suddenly had problems affording their hosting around 2000 because their banner ads suddenly started paying them pennies when they used to provide at least enough cash to cover the server bills.

And that started the trend of websites accepting more and more intrusive ads, because they made more money than banner ads. Pop-ups became popular because pop-ups made money and banner ads didn't.

You're right. Startups are overvalued. But they're still making money. The Indian 'unicorns' - Flipkart, Snapdeal, Ola, etc. have real revenues and customers.

Do they deserve their $1Bn valuations? Probably not. But do they have enough customers to give them $100M-$1B revenues? Yes.

If these startups were public companies, they'd still be valued at at least half of what their last Crunchbase entry says

The ones who are in much more risk are those "selling shovels in a gold rush" - i.e. companies with a revenue stream based on services and products to other start-up companies.

I agree that they have real customer and service. But i think they will still go away. It is definitely a convinience that these service provides but see where Meru or Cell cab and so on... Once the volumes drops it is very difficult to continue these business. I think flipkart still does not make any money and customers are now aware that they exploit or cheat when it comes lot of home appliances and cloth. Most of the items you find on flipkart/snapdeal is priced higher just to show how much discount they give.i had purchased many items they have (non branded (which is about 75%) ) that are shown Rs 1000,50% off Rs 500 and in local market it is priced at Rs 500 and sold at Rs 475 with 5% off. But most people will chose 50% off :(. But slowly flipkart will become a price chcecking website than actual price. Don't get started on appliances and service....

An additional problem is that in a downturn, people reassess what they are willing to spend money on. Overvalued companies with revenues today may see those revenues evaporate. This also happened in the first dotcom crash.

They have serious competition from Amazon and Uber. These are low/no margin, cash flow businesses, surviving on economies of scale. Can they survive a funding crunch? Who knows...

This is what I wonder as well. Uber has grown massively here, but it has managed to do so by essentially bribing drives with incentives and riders with steep discounts.

Once the discounts go and they have to start charging market rates, I wonder how it will affect their prices. At market rates, I don't think most customers here will choose them.

But then again, while a cab company operates at, say, 20% profit margin to break even, Uber can probably operate at 5% margin thanks to its scale.

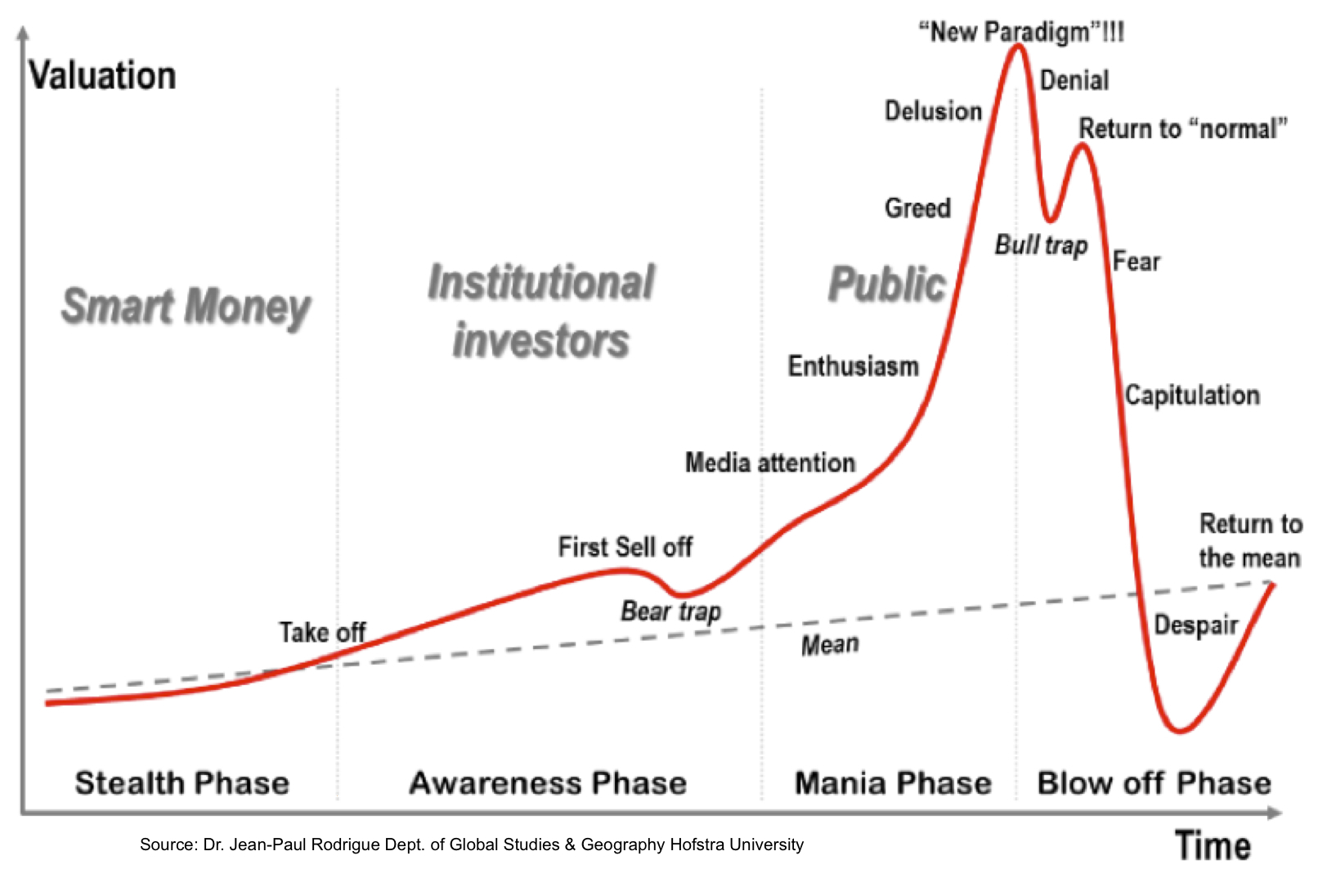

Something of a tangent to what you said, but I see other parallels between current events and 1999 - this is what happens when unsophisticated investors gain sharemarket access for the first time.

It happened in the late 90s in the states (remember those "trading poolside" etrade ads?); it's happening now in China. Only recently you've been able to actively trade and view your portfolio on smartphone apps; it became a kind of game and more and more people piled in. I know people there who were up tens of thousands in paper gains even a month ago and could not be convinced they were basically gambling. Well, they're convinced now :-P

Are you really blaming financial instability on "unsophisticated investors"? Not on automated, high speed traders able to liquidate stocks and topple markets in seconds? Not on reckless, fear-mongering media outlets competing for the most sensationalist headline? Not on government action/inaction affecting trillions in assets?

I think taking 1999 as a general example is a bad idea. The mechanics of how the bubble popped is not really interesting. It could have popped any number of ways.

What happened in the 90s was this. People realized the internet was a huge deal. World changing, re-writing the rules of the economy, among other major human institutions (learning, governance, etc.) They were right. 20 years later a lot has changed because of the internet. Revolutions have been driven by it. Economic titans have been created by it.

A large chunk of the blue chip economy is now made up of internet and internet compliment companies, even Apple & MSFT are in that category. Google, Alibaba. The new blue chips being generated today are internet companies and I'll wager the blue chips generated in 2030 will also be driven by this.

The investors of 1997 were not wrong about the scale of the revolution. What they were wrong about was the importance of early mover advantages. It's as if they expected the internet economy to be built behind walls constructed in their entirety by 2000. They thought they were buying shares in Google, Facebook, Alibaba & Uber, that these companies were all being founded between 95 and 98. Seems silly now. But, hindsight.

The really large scale irrational exuberance lasted a short while, just 2-3 years maybe less. That's hard to justify but it's the end of a bubble when bubble thinking is totally disconnected with the rules outside the bubble.

In that environment, it doesn't matter what bursts the bubble, it's going to burst.

Without that kind of bubble, you don't get that kind of burst. With that kind of bubble, you inevitably get that kind of burst. Investor sentiment may be fickle, but U-haul traffic jams are caused by real economics, not panicky investors.

So, who are these unicorns? Can they survive a month or twenty of panicky investors? Can they do away with investors all together? Are they reliant on investor money for revenues like all the ad selling startups of 1999?

I think no matter what investors do tomorrow morning, Uber, Xiomi, AirBnB and Palantir will still pay salaries, bonuses and such. The IPO might be put off by a couple of years. If the market goes extremely nasty a lot of people who expect to buy houses with stock options will be disappointed. That might cause trouble.

What they were wrong about was the importance of early mover advantages.

There is also a tendency to underestimate the "early mover disadvantage", if you will - if you move too early you risk ending up being little more than a detailed market study for a company that will succeed with your idea a few years later. The current wave of delivery and mobile services includes lots of ideas people were chuckling about in 2000, but now they are functioning pretty well.

I actually have a hard time coming up with an idea from the previous bubble that is not at least being tried again now with more success, or already successful.

I'm not saying someone couldn't do it, but it's not easy.

One classic mockery target is the company that was going to deliver dog food to people. (I want to say Pets.com but it seems like they were more diversified than that.) The only wrong thing about that idea was that it isn't its own company. Amazon will happily deliver you dog food, as well as all kinds of other basic staples. (They even started a new program for that lately.)

Fresh grocery delivery from local stores is probably the best example I have... it exists, we can't quite call it dead, but only in very limited areas, and is still struggling to grow. (Bear in mind that there is a strong correlation between reading HN and being in an area that has grocery delivery. :) It isn't very common.)

I'm interesting in anybody who can come up with something from 1999 that still doesn't exist at all, or has failed so utterly that nobody is trying it today.

Perhaps, but the comparison to 1999 giants is completely nonsensical, IMO.

Uber are breaking records in building a business segment from scratch over an incredibly short span of time. They have been taking investment in order to grow fast. That's reasonable because (1) they have been able to use it to grow fast and (2) this is a business that probably tends to the winner-takes-all end of the spectrum.

Is it riskier than ExomMobile? Yes. Is it a nonsensical investment no? Will they be harmed if all finance markets dry up completely. Yes. Would it kill them? Probably not, but who knows. But, the only reason for a tootle dry-up is if the fundamentals are totally broken, and there is no reason to think they are.

Uber generates revenue. It's business model is pretty solid. Customer like it. This is nothing like the 99 companies.

I think we are in for a tech market correction at some point but I hope it isn't as drastic as the one you paint! Everyone seems so starry eyed in the Bay Area but few seem to remember 2008-2009 when even Google was laying people off. I remember going from being unhappy in my job to being thankful for having one in the span of a few months when pretty much all job postings dried up.

Likewise. I moved to SF right before Lehman, to work at a startup. I had next to no money in the bank when I moved here, and an outrageous rent to pay. It was (financially) terrifying -- but at least it cut back on the douchebaggery in the city!

That said, 2009 wasn't a tech-specific downturn. New York had it far worse than us, and there were still tech companies doing their thing in SF, albeit on a much tighter budget, since the money wasn't flowing. The dot-com crash (which is essentially what I am describing) had its epicenter in SOMA, and we're a lot closer to that scenario than we are to Lehman -- outside of exports (oops, spoke too soon!) and shale oil/gas (oops, spoke too soon!), tech is the primary bright spot in our economy right now. The dumb money is flooding into tech instead of real estate this time, which means that when it does go away, the hangover is going to be pretty wicked.

I got a new job in SV in 2008 as well. People were congratulating me that I managed to get "an" offer. Lots of places had hiring freezes back then. When did things change in the valley? Was it Q4 2010? Q1 2011? I'm genuinely curious and trying to refresh my memory. I feel like I was in a funk and then woke up one day with all this Unicorn talk. Today, housing prices in MV "seem to be" 100% more than what they were in 2010. What the heck happened? Does "Unicorns" explain all of that? Forign investors? Ultra low interest rates??

Q4 2010 feels about right to me -- that's when companies started to hire more aggressively, anyway.

In retrospect, my first "this might be insane" moment happened when techcrunch wrote the "airbnb has arrived" article, announcing that they'd grown a horn and become a unicorn. That was June 2011.

"It was (financially) terrifying -- but at least it cut back on the douchebaggery in the city!"

Don't get it? Personally, I can't find anything positive about spending so much of one's income on rent? If it's crime, my car is still broken into like its 1999?

MongoDB and Gilt Groupe (both of which happen to have been cofounded by ex-DoubleClick CEO Kevin Ryan: https://en.wikipedia.org/wiki/Kevin_P._Ryan) are specifically called out.

Given that it's AGPLed, it unfortunately doesn't look like MongoDB (the joke of a DB) will be going away any time soon, even if MongoDB Inc. (the joke of a company) does.

Systemic shock is likely to be lower than you'd expect, as the Chinese stock market is on the other side of capital controls to the west and so therefore less linked.

I do agree that there's a lot of 1999-like companies around, especially people wanting to do Webvan 2.0.

The feared impact is a systemic Asian downturn crashing industrial export towards the area, which in turn would reduce demand for services. Germany in particular is currently being watched, since their industry relies on export towards Asia quite heavily these days (since European demand is overall low). If German giants start feeling the pinch, the startup world in Berlin will inevitably get hit.

From a US perspective I honestly don't know. Chinese investments are mostly one-way anyway (it's hard to take money out of China) so they shouldn't significantly impact any honest balance sheet; however, if Japan and Singapore start going under as well, things might turn ugly all around.

The scenario you paint is far from sure but possible; but why are you using to comment a crash on the Chinese stock? I hardly see a correlation. There could even be a negative correlation, if more investor money flows back from Asia to the West.

It's important to remember that companies and programmers at the top of their games can still thrive in a down economy. There will always be software to write, especially in economic sectors that aren't directly wired to startups. Take ecommerce for example, which depends on income from the whole population. The whole population never recovered from the last market downturm, yet people still need to buy stuff, and increasingly do so using apps and the web.

I just hope urban real estate doesn't go even more berserk with investors looking to park otherwise uninvestable money.

"I just hope urban real estate doesn't go even more berserk with investors looking to park otherwise uninvestable money."

I fear this too, and I have benefitted greatly from this realestate bubble.

My two hopes are: The Fed doesn't chicken out, and starts to raise interest rates. Plus, I would like to see an immediate end to foreigners buying realestate without becoming citizens first! At least residential? Right now they can pick up a phone, and buy any home.

I know this is supposed to be facetious, but UHAL stock is actually quite attractive at current levels. They own a growing self-storage business but don't break out the profit contribution (although they do disclose the revenue contribution). Pure-play self-storage stocks like EXR/SSS/PSA trade for 18-20x 2016 TEV/EBITDA. If you give UHAL credit for that on the estimated earnings from the self-storage business, you are getting the moving business for a very undemanding valuation despite it growing 5-6% per year and with a dominant market position.

It's very very likely to rebound, but there would be some question of when, and whether that happens before or after your futures contract delivery date.

I remember seeing gas at $4-5/gallon (in the northeast USA), and figuring that everyone should be happier to stock up while it's not far more expensive, and that it's bound to just keep climbing forever as we run out of global supply. Gas is selling for $2.50/gallon or so now, which doesn't mean that it won't climb again and retail for $20 or $100 a gallon in the future, but it does mean that if I bought futures in gas ten years ago for delivery now, then I would have lost of lot of money.

no, the smart thing is to quickly create a startup, uber for uhaul. slick app, shows all available trailer and trucks, you order and they appear in minutes, all transactions done through app.

Yes. The real worry is if this is shared by those outside the tech sector. We can all sit around speculating if the sky is going to fall in without it really mattering, but if it shared by those outside then it can become self-fulfilling.

I don't think we are in a bubble overall. I lived through 1999 and this is not that. But it's possible that there is a bubble in certain "unicorn" valuations.

The question is to what extent these unicorns are leveraged against their possibly-fictitious valuations? Can they survive a collapse of those valuations to more 'sane' levels? One way they could be leveraged is options promised to key employees, all of which would now be underwater.

Of course any company that suffers a valuation collapse and has no cash on hand is toast, since they won't be able to raise on anything other than bend-over terms. So part two of my question is how much cash the unicorns have. If they have enough to last, they'll probably be okay.

Edit:

There are some good arguments against an overall bubble here. Slide 10 with "spending per person online" is a very powerful argument against an Internet bubble but not necessarily against all possible bubble scenarios.

But as I said above, it's possible that there are "mini-bubbles" and that these could pop destructively.

Of course there are other questions, like to what extent are VC firms exposed to China risk and to what extent will stock market losses destroy angel and VC investment? It's possible that the tech field itself is not in a bubble per se, but that it's part of a larger bubble in the global economy.

Yes watch the unicorns. It is the private equity market that will be the place that breaks first. If this dries up then things will go down hill quickly.

I actually think this will be good for the VC industry. Valuations will come back to something based on a universe that is possible and with long term investor (all those locked up limited partners) they can invest with thoughtfulness. It won’t be pretty for the angel investors though.

Not quite right. Interest rates play a larger role all this, which compared to 2000 are at historical lows. The fed might even cut, now. Negative real rates will spur speculative investments.

And small, self-funded, nimble startups outside the valley eat the lunch of overstaffed and overfunded startups with high leverage and a gun to their head.

I don't think we're due another cycle yet, but every cycle just decreases the amount of money you actually need to make a go of it. Sometime over the next 5-10 years another bust would probably be an overall good thing.

Well if you want a prediction for a company that's going to take a huge hit in this downturn: Tesla

They're going to deploy the Model X into a temporarily contracting electric car market, with China upside down, and with the US upper class pulling back spending due to a big drop in asset values. The gigafactory will cost vast sums yet to finish and get functional, and then it'll hit the market with weak demand for several years at least. Meanwhile Tesla's growth on the Model S, which has already stalled out, will get hammered further, pushing their already high quarterly losses even higher - all at time when raising more capital is going to be painful.

Any company that needs a lot of financing to do what they do, is going to get hurt bad through this storm.

Andreesen talked about this. His specifically mentions that many many startups and tech companies are going to evaporate overnight if the capital stops and these are run by people who are basically burning cash and not knowing what they are doing. A major market correction.

...1,968 stocks fell by the maximum 10% allowed by regulators…, or 68% of all stocks in China…

I don't really understand the way a price regulated stock market would normally work. Anyone understand this?

Normally the problem with price regulation is that the market doesn't clear. If the 10% limit was hit, there are sellers out there that tried to get out at the lowest allowable price but failed. Doesn't this mean they are probably going to be shares for sale at a lower price tomorrow?

Any time you hit the floor price you are accumulating a backlog of sellers. I don't think getting a call from a broker that he was unable to sell your shares is likely to cause calm tomorrow morning.

Basically, how's China's regulatory stuff going, now that it's getting tested in rough conditions.

It doesn't work particularly well. A lot of people thought China's management of the economy was brilliant while the growth was easy. The same was true of Putin's Russia while they were riding the temporary oil price boom. Now the tide is going out on all of these easy growth scenarios that were riding the cheap dollar (including the $9 trillion in foreign debt issued in dollars that provided a lot of the growth fuel). The dollar has turned and is crushing emerging markets and pulling trillions in capital away from them.

When the tide goes out like it is now, you quickly discover that the bureaucrats in command economies are almost always incompetent and that incompetence was being temporarily masked.

China was propping up their markets to give the elites time to get out.[1] The stock market bubble was designed to be a wealth transfer, from household savings, to their extremely debt-laden corporations. That transfer is complete, and didn't work particularly well, so now China is prepared to allow the ceiling to cave in on the average investors holding the bag. That's why they've stopped supporting the market.

>When the tide goes out like it is now, you quickly discover that the bureaucrats in command economies are almost always incompetent and that incompetence was being temporarily masked.

So totally unlike those Wall Street genuises, with the trillion dollar bailouts and huge weath transfer crisis...

When one criticizes X (and only X), then -X which might be equally bad gets scot free. That's no logical error, it's a fact (that nothing is said of -X).

So either one does an exhaustive critique of all classes of X, or his critique implicitly favors one of them (it's like if one's two kids do a similar bad thing and he only scolds one of them).

My argument was just trying to bring some counter-balance (to have the -X items people consider as "opposite" to the class of X you criticized, judged too).

The U.S. Economy is to a smaller extent a command economy due to central bank control of currency and interest rates, so it's not 'unlike the U.S..' If he'd talk about the U.S., it'd be 'like the U.S.'.

Doesn't matter how competent you are when the tide is unpredictable. In the long run with each cycle, there is some level of wealth transfer between the developed and developing world and that's not a bad thing in the fast changing times we live in.

Normally the problem with price regulation is that the market doesn't clear. If the 10% limit was hit, there are sellers out there that tried to get out at the lowest allowable price but failed. Doesn't this mean they are probably going to be shares for sale at a lower price tomorrow?

I think that's exactly what's been happening for weeks by now. It's like falling down the stairs - a step each day.

Brent is now $44. Russia produces 10 million barrels per day. Their budget was amended earlier to account for the massive drop from $100 -> $50, leaving a huge hole in the revenues and a massive expected deficit. With a price more than 10% lower than that level, things are about to become really interesting (in the worse sense of the word).

Well, I have a feeling problems will be not so huge as in 2009 due to increased money velocity index, but I can't find statistics behind that (imports shrinked though http://www.tradingeconomics.com/russia/imports ).

- Norway: lots of natural resources, low population, spends only part of oil money (in fact, Norway makes more money per year from the oil fund (i.e., money saved from past oil sales ) than it does from actual oil sales.

- Saudi Arabia: lots of headway to cut spending; standard of living is already very high, with huge reserves to soften the impact of short-term price volatility.

- US: has imported oil for decades until there were enough combined geopolitical and economic incentives to start using its own; exports < 10% of all exports.

- Russia: > 50% of exports are oil; heavily cash-strapped already, so all decreases in oil revenues are directly painful; few options to diversify; too small to be a market maker. Oil money is a direct driver of improving economic circumstances, which in turn provide for much of the countries relative stability.

Norwegian here. The entirety of the earnings from the oil industry is funneled into our Sovereign Wealth Fund, and has been for decades. A few percent (4% ?) of this fund is spent each year by the state. So we are not as hard hit as the others, and the state can basically keep spening money at our present level for many years. Note that oil companies in Norway is scaling back, so our jobless rate and tax income is being hurt, but so far things are only getting interesting for those laid off and those directly in the oil business.

On top of the dwindeling reserve, Russia has been given some stiff fines from international courts for unlawful actions, for example $50bn to Yukos shareholders.

Edit: there certainly are also nations that are in at least as deep problems as Russia, Venezuela for example.

Saudi can just borrow money to help ride things out, their debt-to-GDP is incredibly low (like 3%). That got up to 100% in the early 90s, IIRC, when government revenues had been hurt by a protracted period of lower oil prices.

Saudis have huge cash reserves and can survive on a much lower oil price for longer. The US is already shutting down rigs and other production to get costs in line. As a country the US doesn't require oil exports to stay afloat. In fact, from a strategic standpoint the US prefers to import other countries oil and stock pile its own.

It certainly applies to Norway, Canada, Australia (commodities) and Saudi Arabia as well, among others.

It doesn't apply much to the US. Among the major oil producers, the US is by far the least dependent on the oil market for the domestic economy's well being. It's arguable the US benefits more from cheap oil (industry, consumers, gasoline), than it takes a hit due to the loss of oil jobs and growth in the oil field in general. $40 to $50 oil has slowed oil well expansion and exploration, but US oil production is still sitting near all-time highs, and that will continue so long as oil doesn't go to eg $25-$30 or so for an extended period of time. At a range of $40-$50 for 2016, current projections are that US oil production will expand by another 500,000 barrels per day.

The dollar turning, which has crushed commodities, has pushed Canada into a serious recession, and is threatening to push Australia into one. To make matters worse, China's growth has been trending down for ten years - they temporarily spiked it back up after the great recession at the cost of tens of trillions in debt. China's economy tanking, is hitting any commodity dependent economies very hard.

In Norway's case, they get to start from an amazing position of strength overall. They have extremely low unemployment and a very high standard of living. They have the sovereign wealth fund to lean on if times get really bad. It's very likely that five years of cheap oil will hit Norway very, very hard. They're already facing a scenario where they'll have to tap the sovereign fund to deal with their budget demands. That's not going to get any prettier any time soon. The party is over, but Norway has a lot of wealth accumulated from it, and can weather this storm better than most.

Saudi Arabia has $640+ billion in foreign reserves that they're depleting by the month. It'll get worse over the next year, but they can weather it for a few years yet without a threat to their stability or economic well-being. Saudi is of course also among the low cost leaders on production, so while their budget demands $100 oil, on the other side they have among the best margins on what they are producing.

Out of the group, Russia is drastically worse off. Not only have they been trying to significantly increase military spending at exactly the wrong time, not only are they under international sanctions, but they're starting from a position of national weakness compared to eg Norway: their people are not well off, their Ruble is being hammered, and they're run by a dictator that is not good at managing the economy (as witnessed by their complete non-diversification the past decade plus, which has left them vulnerable to this outcome in the commodity market).

I almost entirely agree with you, just wanted to add a bit more colour to your comments on Canada and Saudi Arabia.

Canada is clearly in recession but I don't think we can call it a "serious" recession yet. So far more of a mild contraction (but pretty terrible if you focus in on energy). I do think the rest of the economy is lagging behind energy and bad times are ahead overall, especially with so much of Canadian growth/prosperity tied to the housing boom. I'm probably preaching to the choir here, but seriously: when the prime minister promises a home renovation tax credit during his reelection campaign - and explicitly states he's doing to help boost the value of Canadians' homes - you've gotta know people are captured by the real estate boom narrative.

On Saudi, they can afford low oil prices for a while and can just borrow if they need to. Super low debt around 3% of GDP, low cost basis as you say, and they've done this before and come back from it (100% debt-to-GDP in the 90s o the back of low oil prices). I've seen interesting speculation that Saudi is willing to hurt a bit from cheap oil because it'll hurt an increasingly-economically-integrated Iran more.

I agree with alot of what you have said. However, here is what I am trying to understand. Who will buy US treasuries, when all its major buyers are getting in serious trouble? How will US government fund itself?

Russia walks the thin line - large population, huge social spendings, military spendings also, restrictions on borrowing cheap capital. Might be first to fall.

Makes me really want to move my savings (which are already in dollar mostly) out of Russian banks, but I'm not entirely sure where to. Or just burn those on something?

If I were you I would def move it - can you get to london and setup an account there? Just look at Argentina - when they went broke they converted all foreign currency accounts to pesos (at terrible rates) - effectively stealing large amounts from the people

Huge trouble? While there is an economical slowing in the oil patch, exactly as expected, the government most recently posted a surplus.

Canada is a bit odd relative to oil given that a pretty large contingent of Canadians are really on the fence about exporting fossil fuels. Even in Alberta, the province where most of the oil action happens, the provincial government was recently taken over by a party that you could almost call anti-oil (to the limits of pragmatism).

Huge might be an exaggeration, but Canada is in a lot of trouble.

1) Six of the last seven months have seen economic contraction. There's no reason to think that's going to get better soon, given what's happening to the global economy, China and commodities. Oil has continued to get cheaper, commodities have continued to go down, and China's economy is getting sicker.

2) Canada's real estate bubble will be popped by the recession. That'll make the damage a lot worse. The constantly rising housing market was contributing temporary, artificial growth to the economy for the past decade.

This is going to be a drawn-out downturn. China is going to have an extremely difficult ten plus years due to their debt burdens, and the fact that all the easy growth ended years ago. The historic cheap dollar years from 2002-2014 are not likely to return, the high dollar will continue to put pressure on commodities, and countries dependent on commodities. Canada won't grow again unless the dollar drops, or the global economy booms, either of which would send commodities higher.

I replied to someone claiming that Canada was in "huge trouble". It isn't in huge trouble. You have provided conjecture, but the truth is that it's exactly the same conjecture we've been hearing for around 15 years. By that reasoning, Canada has always been in huge trouble.

Most commodity prices are doing superbly (oil is an outlier). Food prices are at all time highs. Canada's economy has faced far more of a disruption from normal globalization and mega companies shifting production elsewhere, than any hewer or wood miner of minerals disruption. It will always face threats and will always be adapting.

It's not the same conjecture. It's a fact that Canada is in a recession right now. Their economy is highly dependent on the price of commodities. The price of commodities is primarily determined by the dollar and demand. The dollar is high and is going to stay there. Demand is toast. It's obvious what outcome that is going to spell for Canada.

Nearly all commodities are lower than a year ago, and half of them have crashed. Oil is the opposite of an outlier.

Copper has gone from $3.30x, to $2.20x in a year. Copper is considered a critical bell-weather commodity. Demand for copper has fallen off a cliff.

Iron Ore has crashed by 60% in less than two years, and is down 40% in just one year.

Coal has dropped by over 20% in one year.

Steel prices are down 30% in one year.

Platinum has gone from $1500x to $992.

Natural gas was $4 last year this time, and it's $2.60x now.

Heating oil and gasoline have crashed with oil.

Sugar has dropped by 50% in a year, on a non-stop crash.

Lumber is down by 1/3 in a year, and has crashed.

Coffee is down by 40%.

Corn, wheat and orange juice are all down slightly versus one year ago. Rice is down about 15% vs a year ago. Soybeans are down 13%. Soybean oil is down over 20%.

I was under the impression that BC and Alberta were natural resource economies which don't deal well with a high US dollar, but Ontario actually does well with a high US dollar. Also, a high US dollar makes US out-sourcing to Canada (as well as film industry on-location shooting) a great value.

What threw Canada into a recession, is that they don't have enough other export offsets against the commodity & China weakness. They haven't managed to diversify their economy much in the last ten years. It has become an active topic of discussion since their economy began contraction, with everyone throwing around blame. So while the loonie has taken a hit [1], that isn't going to bump exports very much.

Well, after a big dip when the US markets opened (the NASDAQ was down by more than 8% at one point, and the DOW dropped 1,000 points at the open), they've recovered and stabilised down between 2% and 3%. European stock markets have recovered from their lows too.

Looks like it's time for the first real-world test (for most of us younger folks who didn't have anything invested in 2008 and have enjoyed a bull market since then) of all the theories I've read from financial independence gurus about index funds, i.e. how the market always recovers and goes up and if it doesn't none of this will matter anyway, the financial heads will always say it's different, the investors will always panic and oversell, just stay tough, hold on, maybe buy more, and come out ahead...

China's market is very different than the markets in the developed world for a number of reasons (more isolated, less mature investor base, more direct government involvement, to name a few). So it probably isn't the best barometer for how other markets work.

The stock market operates differently, but China's economy, which is an integral part of the world economy, is still tied directly to the market.

Chinese economic fundamentals (export, import, saving, consuming, government spending) will all be impacted by a failing stock market, which will translate into economic concerns across the globe.

Allow me to barge in with my armchar financial analysis ...

If you check the Baltic Dry Index , it's started dropping in the past few weeks indicating a slowdown in global shipping. Similar for crude prices.

There was a similar pattern in 2008 (though the reasons this time are a bit different) with crude and the Baltic index starting to tumble in August before the market nosedived in September. Not that we will repeat 2008 but we definitely have a leading indicator for renewed weakness in the global economy.

Honestly, the BDI hasn't really changed that much as compared to the 2007 heydays : http://investmenttools.com/futures/bdi_baltic_dry_index.htm . There was some increase in the 'green shoots' days, but it's been bumping along since then. If anything, I think that means the world economy hasn't really ramped since then. Still, I'd love another opinion by someone that recognizes the value of watching the BDI.

It's far worse than even the baltic is indicating:

"Shipping freight rates for transporting containers from ports in Asia to Northern Europe fell by 26.7 percent to $469 per 20-foot container (TEU) in the week ended on Friday"

"It was the third consecutive week of falling freight rates on the world’s busiest route and rates are now nearly 60 percent lower than three weeks ago."

Not suggesting that you're wrong, only that you're lucky: there is always a risk that things go in any direction.

If you're in it for the long haul, selling your ETFs a month ago isn't necessarily the best thing to do – at least by virtue of allowing yourself to sell your stocks when you feel it's the right time, which is mostly going to be dead wrong.

And selling them today is certainly a terrible idea.

Is that surprising at all? If we take a look at the Shanghai Composite index in the past 5 years the bubble is pretty obvious [1]. That makes me wonder whether a simple averaging/smoothing law could mitigate such crazyness without limiting sensible business traffic significantly. I don't know enough about the stock market to say how and whether this could work, but the fact that a monstrous apparatus like this is allowed to develop such abnormalities seems absurd.

It's not exactly simply "being allowed", China has been implementing a lot of new measures regarding this crisis (e.g. banning short selling, limiting price drops). Some people argue those have been making it worse - though for a layman like myself, it's hard to distinguish honest from biased opinion.

Averaging of what? Prices are what they are, despite limits on daily movements (closing "limit down"). Price controls can work on commodities in some limited circumstances but not on a pure abstraction like a stockmarket.

I recently decided to hold on to my stock (Netflix, Adobe and Philips) for a while, since advice was still mostly positive. I guess I should check how that's going.

Edit: I did. Fuck.

Though in all honesty, I don't see why a correction in China would seriously hurt the profits of Netflix. Maybe I should buy more.

I could see Netflix doing better in a recession, a few bucks a month for the entertainment it provides vs the cost of going to the cinema (two good cinema tickets here costs ~4 months netflix subscription).

Perhaps a more accurate description: provides entertainment vs the cost of a cable subscription. Plus, recession or not, they are riding the wave of chord cutting nicely.

Actually you would think this would be true, but because of the cost of holding a position you can lose money if the market stays flat (not likely given the current VIX).

Write options that are barely out of the money, buy options that are way out of the money. That'll limit the size of the pennies you pick up, but can also limit the size of the bulldozer.

In 2000 this best trade was not to short stocks (too hard to time) but to go long safe haven assets (treasury bonds) for a much smoother ride. However this time around that might not work with the Fed wanting to raise rates(which would hurt bonds).

It might exactly work because a rate raise is expected. That way, you can make a gain twice. First due to the flight into safe haven assets, and then again when the raise hike is postponed again and again. (Just a scenario. :) )

Does anyone have a good link to a quick refresher on fundamental analysis and/or a reading list besides Graham and Buffet? Seems like just about the right time to look over some financial statements/balance sheets in depth.

Stop. Most of my life savings are still in yuan. I really need to convert the rest. We converted a bit when the first devaluation happened (my wife can do that since she is a citizen), but to do the rest, I have to wait a month for tax receipts from work....the joy of earning money in an inconvertible currency!

At least you live in a country with significant internal production, so overall things shouldn't get too bad for you even after devaluation (as long as you stay in the country and buy Chinese).

I grew up in Italy during the last few devaluation waves and then the Euro switchover (when prices basically doubled overnight) -- prices of everything except food and shoes skyrocketed, it was really ugly for us little people.

In short, some specific sectors did increase prices dramatically in those years, and probably were the ones felt the most by everyday consumers (food, restaurants, retail etc). I would personally add that Italian statistics on economic elements are historically lacking, due to widespread tax evasion and unreported activity, and suffer from the huge economic disconnect between North and South.

Buy what? Overpriced apartments and cars? I go to the mall and see nothing very interesting, imports are already very expensive, even made in China goods are expensive, I mean 800 RMB for a pair of Levi's wtf!? The only cheap things are food and taxis. I do most of my clothes shopping on trips back to the states to save money.

You're in a very tough spot (you already knew that, I hope). One way you might get it out a bit quicker is to offer someone who has cash abroad already a percentage, but it's going to be very hard to find takers.

I'm not panicking yet, it's just on my to do list. I think the gov will try to keep the currency stable, because otherwise there will be lots of panick. The stock market is one thing, few people are exposed to that, but most people have huge savings in cash; there would be riots if they go to 7 since the weakness would lead to price increases.

I'm curious if you could buy Bitcoin on one of the Chinese exchanges transfer it to an exchange out of the country and sell it for Euros or US Dollars?

The first devaluation is just a political move. Just to test the waters - will the Americans go crazy about them devaluing.

In the second act, they will say - hey, this 1.5% didn't work. Look our industrial production is still falling. We have to adjust to market forces and devalue more. Then comes the 20% or so devaluation. But look, the Yuan has appreciated around 8% the last 5 years, so it will only be a relatively small devaluation. That will be the argument.

My expectation is VC money is less likely to be affected than the private equity funds. VC funds are pretty long-term and the the limited partners are locked in tight. It is the unicorns looking to raise money out of the private equity market or IPO who will really struggle if the market turns.

It would be hard to spend even a day in Shanghai and believe that the system you're observing is "communism", even under the notoriously wide range of meanings people have assigned that term. Something like "state capitalism" is a decent description I think.

I think it's obvious he's talking about China as a country that has a capitalistic economic infrastructure with a communist social ideology & political structure.

Isn't the core part of communist social ideology that the government should constitute the political rule of the proletariat? I'm having trouble finding aspects of China's social policy that looks particularly communist. Their policy in the social realm is something like: try to minimize social upheavals, and keep huge and growing inequality from causing open rebellions. When useful, distract the population with nationalist red meat. All that seems like pretty normal fare for an authoritarian capitalist country.

Because of their embracing of the free market, it's often accepted that China is not a communist nation (despite being led by a communist party).

Actually, this situation is pretty much just capitalism at work. It really has nothing to do with communism; every free market is susceptible to this sort of failure.

It's anything but "capitalism at work" if "capitalism" has anything to with "free markets". The Chinese Government has been graying out, if not altogether fudging, their economic indicators and propping up domestic investors. Now it has moved to outright rigging of the market through selective bans and directives (no short selling, no selling if you hold >5%, no trading at all on certain stocks, and so on).

This current rout is simply a continuation of the previous one in July when similar curbs were placed to halt the plunge.

Once again, even if their tactics work they'll only help bring about yet another plunge.

All in all, the western demand is dying out since most countries are trying to in-source materials and goods (instead of importing from China) and domestic asset bubble has nowhere to pop and the lies invested in that bubble have nowhere to hide.

That was not my point. I am being critical of China for staunchly supporting Communism (and hence to some extent being anti-capitalism and anti-democracy) and at the same time reaping benefits from democracies and capitalist states. I guess HN didn't like my earlier comment, but I do believe that. China has several times castigated India (where I belong) for being a shoddy nation of scared people due to its democracy. I find it a double standard.

> A communist nation trying to reap benefits of capitalism

Thank god that US companies will never betray their nation's core values by shelling out to non-free countries in order to save production costs and circumvent labor laws.

Actually, China goes way beyond that. Where the U.S tries to nudge things one way or the other indirectly (by changing interest rates and the like), China has total control over their economic & monetary system (including the banks). And they exert that control almost daily. It's one of the reasons why the Chinese Yuan will replace the dollar as the world's reserve currency.

I think the US and the UK interfere plenty. At least China isn't pretending they are against central control whilst pumping out "free market" rhetoric.

China has vaporized trillions already trying to bail out their banks, which are extremely over-leveraged on debt. China's entire banking system is under high duress right now due to the 'shadow banking' debt mess.

{kind=link}

{kind=link}

{kind=link}

Unable to raise further "growth capital" at attractive valuations, and burning money like there's no tomorrow, we see the first unicorn layoffs within 3 months. This spooks investors further, which dries up whatever funding was left for early stage deals. Within 6 months, the weakest startups are beginning to fail outright, which pulls back the tide a bit, and reveals the ponzi scheme of startup-servicing-startup revenue cycles for what they are. Suddenly, a number of heretofore assumed "safe" investments with "strong" revenues are revealed to be precarious, as 95% of their revenue streams were correlated.

Companies go from healthy revenue to practically nothing overnight, as dozens of companies all cut back on burn simultaneously. This only exacerbates the cash flow problems, and startups that were flying high are now flying into the ground at remarkable speed. Market gurus are revealed to be wearing no pants.

Within a year, the valley is in full recession, and people are clamoring for U-Hauls out of San Francisco, which are in short supply...

(In case you were wondering, this is essentially what happened in 1999, minus a few wild-cards like companies with totally fictional revenue, and companies that had no revenue at all.)